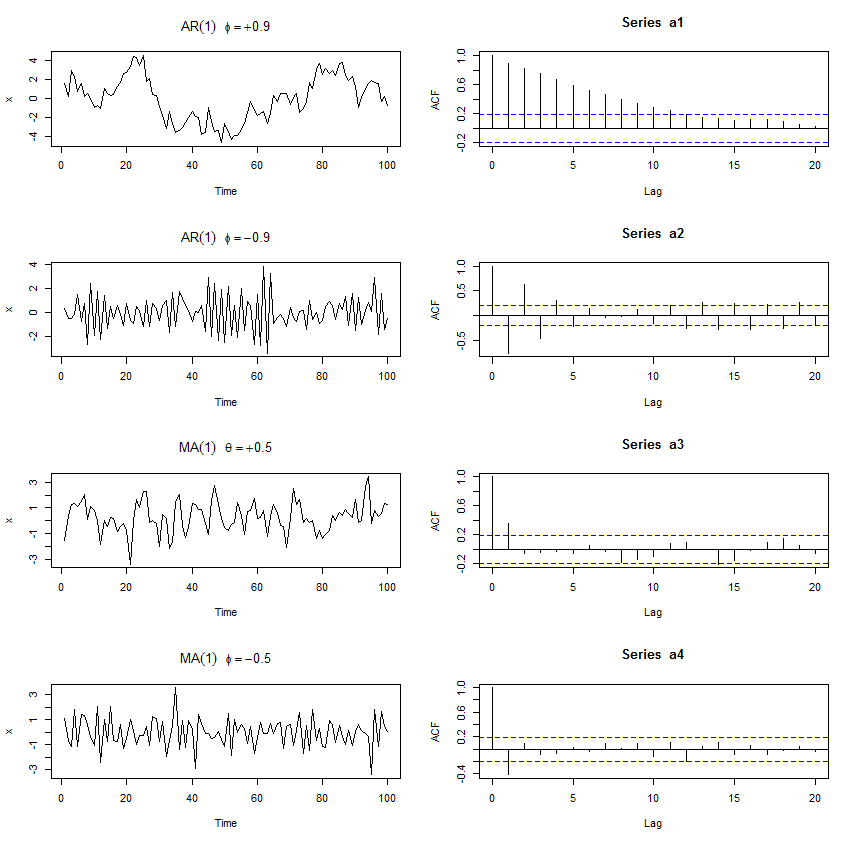

ACF of AR(1) is phi^h

ACF of MV(1) is theta/(1+theta^2) only for h=1 and 0 when h>1

——————————————————————————————–

par(mfrow=c(4,2))

a1 <- arima.sim(list(order=c(1,0,0), ar=0.9), n=100)

plot(a1, ylab=”x”, main=(expression(AR(1)~~~phi==+.9)))

acf(a1)

a2 <- arima.sim(list(order=c(1,0,0), ar=-0.9), n=100)

plot(a2, ylab=”x”, main=(expression(AR(1)~~~phi==-.9)))

acf(a2)

a3 <- arima.sim(list(order=c(0,0,1), ma=0.5), n=100)

plot(a3, ylab=”x”, main=(expression(MA(1)~~~theta==+.5)))

acf(a3)

a4 <- arima.sim(list(order=c(0,0,1), ma=-0.5), n=100)

plot(a4, ylab=”x”, main=(expression(MA(1)~~~phi==-.5)))

acf(a4)