There is this fantastic TV show Shark Tank from ABC, where startups come to pitch their business to a group of seasoned businessmen/women. The “sharks” will decide if they should invest their own money in those startups, hence, their motivation is to seek for high return and the questions they asked are usually challenging. I have always been asking myself how can the sharks invest that much amount of money, usually hundreds of thousands of money for partial ownership – equity within just a few minutes, and one step further, how can they even tell how much a business worth in the first place? Sometimes, they call out the entrepreneurs “crazy” valuation and sometimes they take the offer the way it is, and sometimes even go beyond what was originally asked.

After watch it for a few seasons, you started to see patterns where they pretty much want to understand their income from revenue, margin (in order to calculate gross profit) and net earnings (take home). Relatively speaking, not that much questions about balance sheet or cashflow. Clearly, their valuation are based on those key financial metrics, but the question is how do they go from those metrics to how much a company worth? Thanks to some of the heated conversations every now and then, the sharks will make similar comments like “you are asking for a valuation X multiple of your earnings, you know that will never happen in Y industry, right?”.

Then you have been told the secret, the next question will be WHY a company’s worth is a multiple their earnings and why that ratio is different across industries?

To determine how much anything worth, there are usually several ways, what is the cost, what is the worth of similar product that have been sold recently, and if you ask someone in finance, they probably will threw you off by saying “the current worth of an asset is the sum of all its future cashflows discounted to today”.

Lots of buzz words, right, “cashflow”, “discount”, “asset”..etc. Do not worry, everything should be pretty straightforward after we go through a every day example.

First is to make sure that we are all on the same page that “one dollar tomorrow is not the same as one dollar today”. This is called the time value of money and can be explained using your interest paying saving account. Say you have a very good bank with an interest rate of 10%. There are lots of details go into how actual interest (yield) could different based on when interest are paid and how often are paid, let’s put it on the side and assume $10 is paid the end of the year if you put $100 at the beginning of the year. The you will have $110 at the beginning of next year and 10%*110 = $11 worth of interest will be paid end of the next year, interest will get higher and higher thanks to the interest built on top of earned interest, everyone favorite compounding. So your $100 dollar today look like “worth more” in the future.

Year 0: $100

Year 1: $110

Year 2: $121

…

Year N: $100*(1+10%)^N

However, in nature, they are same because you take no risk in this investment since it is the bank (I did not go through 2008 so bear with my naiveness here), you do not have to do any work other than providing capital, last, this kind of investment is open to pretty much everyone. Therefore, any reasonable investor shall “take this for granted” if they decide to park their money somewhere else.

If someone is going to ask you to invest or borrow your money, you should expect they pay you back higher than what they borrow you today, or vice versa, you should expect to lend out lower if they promise to pay you back a fixed amount in the future.

From another perspective, $100 next year will equal to $91 today, the same as $110 to $100 in the previous example; $100 two years will equal to $83 today, the same as $121 to $100. Now, we are ready to look at how a company will generate money for its investors.

A company will bear the goal of making profit, making profit to keep its day to day operations (if not, they will not live long), sometimes even to have some profit after paying for all kinds of expenses which is called the net income / earnings. Earnings sometime are reinvested back to the business to scale up its success and sometimes those extra money will be given back to its investors. Of course, depending on the stage of the company and its potential based on various reasons (industry, business model, environment, ..etc), investors will expect different use of those earnings, that is also why some companies pay dividend up to 10% and some tech companies pay literally no dividend. Let’s say the business that go to shark tank is already operating, has already attracted a fixed group of the customer with returning business, the revenue pay for everything with extra. If I am the owner of this business, we can start by assuming all earnings go to our pocket. Let’s even fixed everything else assuming that from now on, they company will make same amount of earnings ($100K) every year for the future. In that case, it is a pretty good way of collecting cash in the future. Using the idea we mentioned, let’s try to convert all those future annal net income to today’s worth. Shall we use the interest rate above? I will say yes for now, for in reality it is probably not this simple, the risk of running a small business is high, you probably will need to put into effort, so you probably should expect an return rate higher than bank interest.

Year1 -> today: $100K / (1+10%)

Year2 -> today: $100K / (1+10%)^2

Year3 -> today: $100K / (1+10%)^3

…

YearN -> today: $100K / (1+10%)^N

In order to give away this cashcow to you, the entrepreneur probably will trade you fairly at the price of receiving the same amount of the money in the future.

So sum will be a very simple geometric series where the sum can be represented in the following equation:

valuation = $100K/(1+10%) * (1-q^n) / (1-q) where q=1/1.1=1/(1+rate)

Now that we know the magical multiple is pretty much

valution/earning = (1+r)(1-1/(1+r)^n)/(1-1/(1+r))

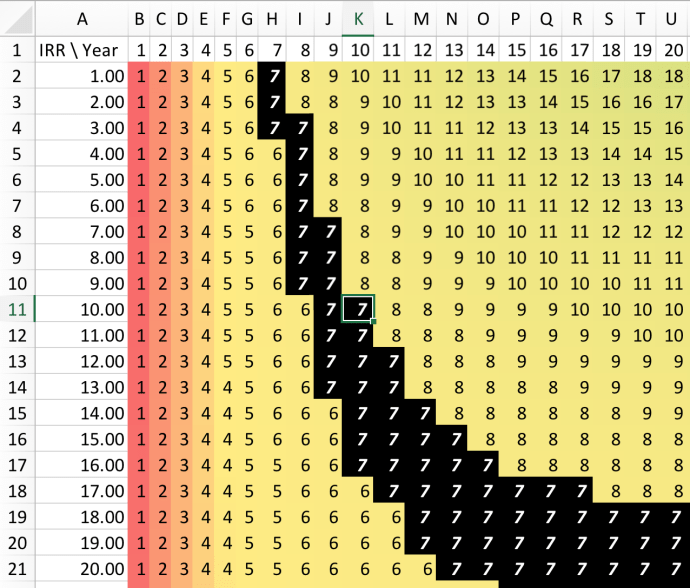

I plot out a heatmap based on “multiple” using the number of years and IRR (internal rate of return). The interesting pattern is that as the rate increases, the multiple caps at certain value, the higher the rate, the sooner it flattens and the lower its cap is.

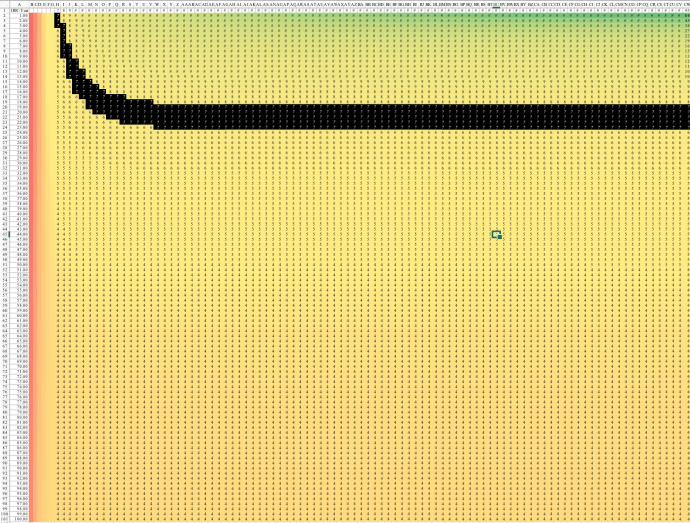

I also expanded the limits of each variable from 1 to 100 and here is the bird view.

As an investor, I might ask myself the question of how long this business might keep making money for me (dividend or capital gain due to reinvested earnings), what will be my required rate that I will expect taking the market interest rate and the premium that I want to add on top of that.

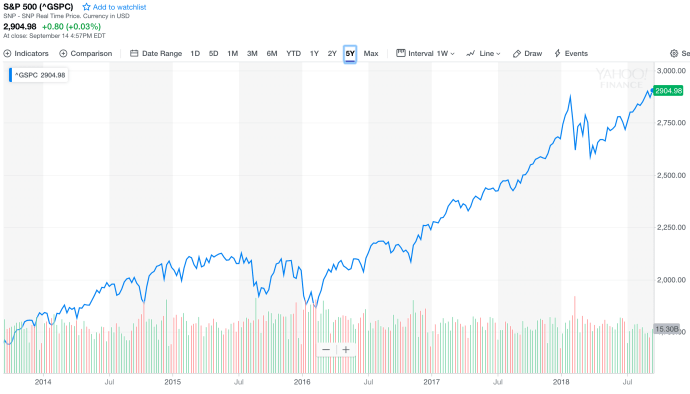

One can easily tell that the bank rate for investors is usually the big index funds and S&P 500 has already achieved an annual return of ~ 11%. If we double that benchmark to 22% as the required rate of return. Then we can see that by holding the company forever will earn no more than 7 times the original investment. Again, the power of compounding, $100 in 7 years will only worth $25, $5 in 15 years and roughly $1 in 23 years.

As you can see, if your business is attractive enough that your investor believe whatever you do will keep existing forever, also, if you can convince your investors that your business is less risky and at the same time, there is no good equivalent on the open market for investors (low interest), then you will position yourself to the top right of the chart. Of course, this article is based on a strong assumption that the earnings is fixed which it is never, it either can operate only for a few years (less than half of the small business survive the first 5 years), or the earnings could be volatile upwards and downwards for various reasons.

But in the end, hopefully this article is helpful to understand how a company worth from the most basic perspective and what are some of the factors investors and entrepreneurs need to pay attention to fairly evaluate and determine a company’s worth.

Part words from Shark Tank again “in sales, we trust”

Credits:

- SharkTank from ABC, screenshot, comments, copyright reserved to the original author.

- Yahoo Finance