EPS (earnings per share) is a very important ratio in income statement, it is calculated as earnings (net income) attributed to common shareholders divide by common shares outstanding. Actually, it is so important that it is required to include EPS on the face of the income statement.

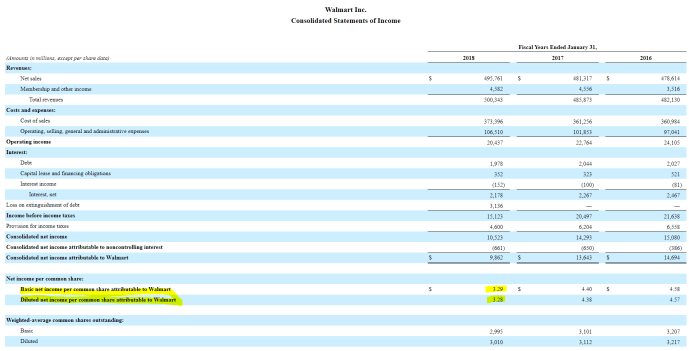

As you can see, they not only show the EPS, there is also another line right below it which is the diluted EPS. The reason that diluted EPS need to be disclosed to the public is that there are different kinds of equity like preferred stock, convertible stock that has the potential of “diluting” the EPS. How big a difference is can be? Usually it is pretty small, like for Walmart, the earnings per share is only 0.01 but in some cases, the difference can be material enough that investor want to know the potential downside.

Say for example, convertible stock sometimes got paid dividend and can also be converted to certain amount of shares. If not convert, that is the simple calculation for EPS, however, the diluted EPS to evaluate if all the convertible stocks got redeemed into common stock, on one hand, the net income will increase because the earnings that used to go to dividend now can be retained, on the other hand, the number of outstanding common shares also increased due to the conversion. In this case, there is a scenario where the diluted EPS if converted can actually be higher than the basic EPS, if this happens, the diluted EPS sort of loses its meaning of providing a good projection of the potential downside. Both IFRS and GAAP require that this kind of EPS – Antidilutive Security be excluded from the diluted EPS calculation.

Now, let’s do some simple calculation and see under what situation Antidilutive security could exist.

Say a company’s net income is I, number of common shares outstanding is C and number of preferred stock is P. The term for preferred stock is that the annual dividend paid per share is D and it can also be converted to X amount of common stock if wanted.

Basic EPS = (I – P * D) / C

Diluted EPS = I / (C + P * X)

The constrain is that Basic EPS >= Diluted EPS

(I – P * D) / C >= I / (C + P * X)

After a bit transform, we got: X*I – D*C – P * X * D >= 0

I like to rearrange it into the following format:

D <= I / (P + C / X)

This is easy to interpret, P+C/X can be interpreted as if all shared got converted into preferred shares. If the dividend is smaller than if all converted to preferred stocks, then it is dilutive. If not, then it is anti-dilutive which should be excluded. So in this case you can see, if the dividend for the preferred stock is too high, or the conversion X is too small, it is highly likely that the constrain will not hold and it will be anti-dilutive. Also, if the number of preferred stock is substantial, this will also become anti-dilutive.