Background

Countries impose taxes to maintain its operation. Different countries have different tax systems. When cross-border business happens, it become more interesting. In order to for an income to occur, it usually includes two “where”s – one as where the income was originally sourced, aka. where the money was made, and another one as where this successful business owner resides.

There are countries which taxes all incomes incurred within its boarder is claimed to be source/territorial tax system. On the other hand, countries could be tax based on business owners’ residency, for example, it might not tax aliens but at the same time, it will impose taxes on its own citizen’s foreign income – residence tax system.

If you are unlucky, you might have to pay tax twice, maybe because your business happens to qualified as sourced from both countries, maybe because of your duo citizenship, or as your income got taxed when it was sourced in one country, and also a different country where you reside impose another income tax again afterwards – that is called double taxation.

Usually countries work together to mitigate this effect, where the money got sourced usually take the first cut, and then the residence country will provide some tax code to accommodate. In this case, the source country will tax its own fixed amount say 40%. How much extra its own resident should pay will be calculated in three ways: credit, exemption or deduction.

Foreign Tax Credit Provisions

Exempt is the most straightforward as if its resident paid income tax to its source country, then there won’t be any further taxation – simple and straightforward.

Under credit method, one will pay the residence country the amount which residence tax is higher than its source. If the source is 50% and residence is 20% only. No need to pay more tax after you got taxed 50%. However, if the source is 20% while the residence is 50%. One still needs to pay the delta of 30% to its own residence country. One way or the other, the residence country need to maintain the total tax rate as being max(T_source, T_residence).

Under the deduction method, it is just like various types of individual income deduction from medical, car tax. The residence country will only tax on the portion post tax. so it will be T_residence * (1 – T_source). The total tax rate will be T_source + T_residence * (1 – T_source) = T_source + T_residence – T_residence*T_source.

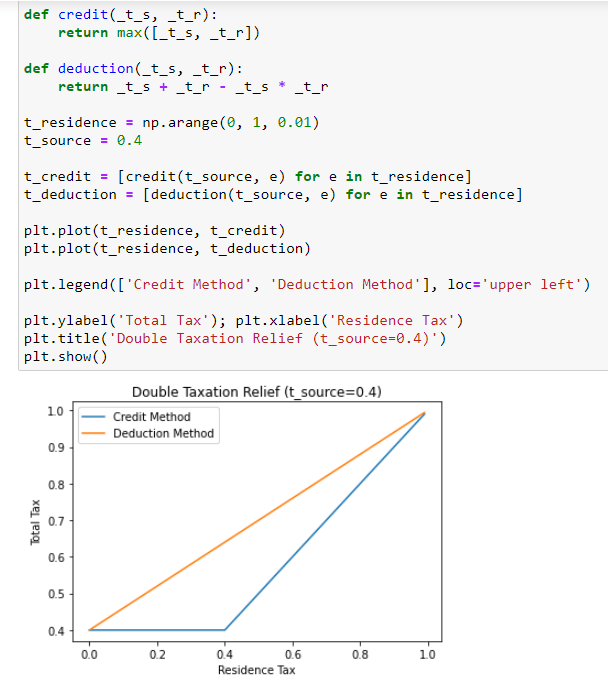

So let’s take a look at an example, if we hold T_source to be a flat 40%.

Under the credit method, the total tax rate will be max(T_residence, 40%) and under the deduction method, the total tax rate will be 40% + T_residence 60%.

Example – Credit better than Deduction

one interesting observation is that the credit method is always more effective for the same amount of source tax rate.

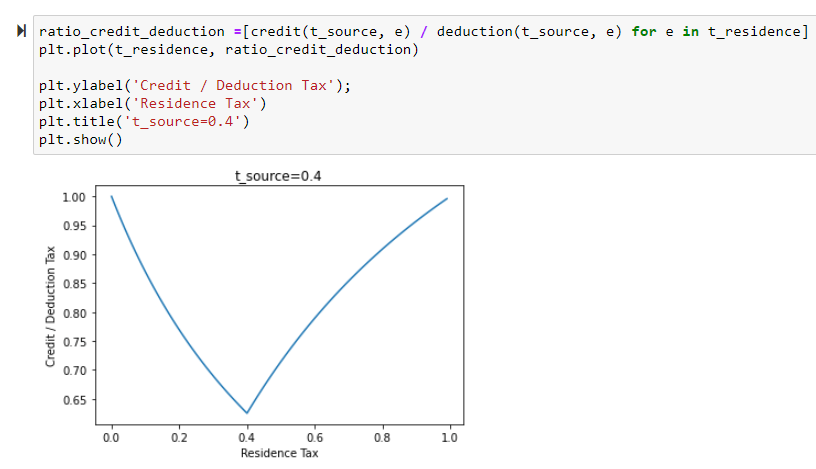

And if we plot the ratio of credit vs the deduction method.

We can see that the credit method is always lower for the tax payer and the marginal benefit is the highest when the residence tax equals to source tax. That being that, when the residence tax is extremely high or extremely low, both methods converges to T_residence which is not a surprise after all.